Delhi ITAT rules that payment made by assessee (Indian subsidiary company) during AY 2000-01 to 2006-07, to its German parent towards intranet charges and SAP software, amounts to royalty under the Act as well as Article 12 of India-German DTAA, however quashes assessment u/s 201/201(1A) for AY 2000-01 and 2001-02 made beyond 4 years following Delhi HC ruling in NHK Japan; Notes that in present case, payment was made for use of SAP software which was customized for the group, further notes that payment was made for use of licensed software on the Internet/ intranet which was contingent on the number of the user licenses or number of sessions for which the software was used; Also notes that the technical support would be provided by SAP, a German company and not by the recipient of the expenditure, accordingly ITAT holds that the software receipt is ‘scientific equipment’ under the Act and DTAA and falls under the ambit of royalty; Rejects assessee’s contention that the amount paid to its associated enterprise was only reimbursement of expenditure, notes that assessee neither produced any agreements, contracts, debit notes or working of such reimbursement to substantiate its claim, clarifies that “If the expenditure are incurred by the assessee and same were paid by the associated enterprise on the basis of the actual charges pertaining to the assessee, then only it can qualify as a reimbursement of expenditure.”; HC remarks that “If the contention of the assessee is accepted and the payment to third party, routed through its holding co. is considered as reimbursement of expenses to the related party, then probably all the relevant provisions in this regard will become redundant.”:ITAT

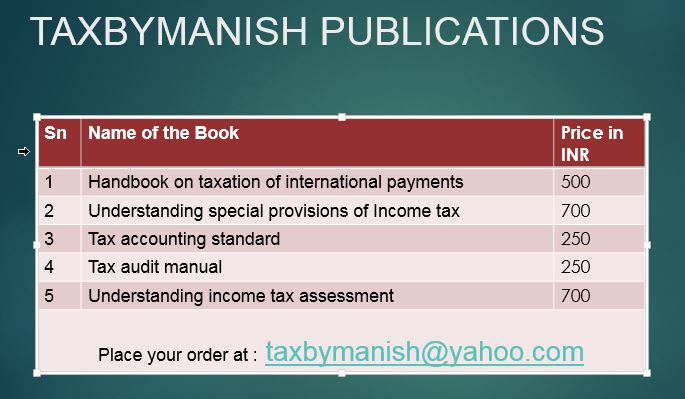

e mail your querry at taxbymanish@yahoo.com