The way forward pursuant a recent advance ruling holding that remuneration paid to directors is taxable under GST, on reverse charge basis, in the hands of the Company:

Continue reading “GST on Director Remuneration – Way forward.”

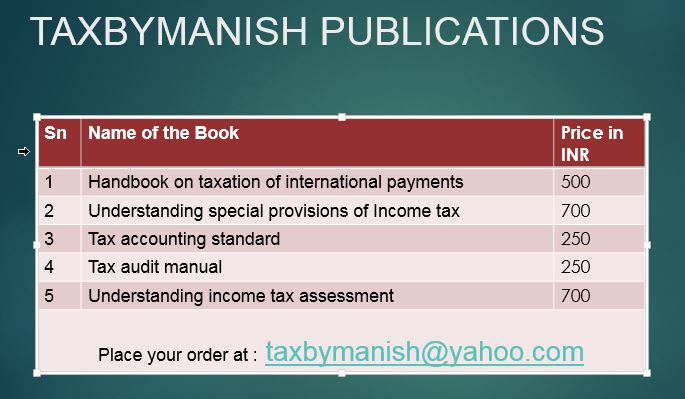

e mail your querry at taxbymanish@yahoo.com

The way forward pursuant a recent advance ruling holding that remuneration paid to directors is taxable under GST, on reverse charge basis, in the hands of the Company:

Continue reading “GST on Director Remuneration – Way forward.”

This Alert summarizes various new proposed labor codes, provident fund and other employment related updates on account of COVID-19. Continue reading “New labor codes, provident fund and other employment related updates on account of COVID-19”

This Tax Alert summarizes recent instructions issued by Central Board of Indirect Taxes and Customs (CBIC) regarding processing and disposal of all pending refund and drawback claims.

Background:

BACKGROUND:

The Finance Ministry in view of the COVID-19 outbreak announced various reliefs relating to statutory and compliance matters under Indirect Tax. One of the major relief given to the taxpayers is w.r.t. availing of Input Tax Credit [“ITC”] under the Goods and Service Tax [“GST”] law. Continue reading “Deferment of GSTR 2A reconciliation for availing Input Tax Credit”

Taxpayers (“Corporate Debtor”) undergoing the Corporate Insolvency Resolution Process (“CIRP”) under the Insolvency and Bankruptcy Code, 2016 (“IBC”) have been facing difficulties due to the inconsistencies between the provisions of the Central Goods and Services Tax Act, 2017 (“CGST Act”) and the IBC. Continue reading “Registration of Corporate Debtors under IBC.”

Income-tax laws (ITL) empower the Tax Authority to give a certificate of lower withholding/deduction or collection of taxes (LDC) if the Tax Authority is satisfied that the total income of the recipient or payer, as the case may be, justifies withholding/ collection of taxes at a lower or nil rate[2]. For obtaining such LDC, the taxpayer is required to make an application before the Tax Authority in prescribed form[3] through TRACES portal[4] with digital signature or electronic verification code. The Central Board of Direct Taxes[5] (CBDT) is authorized to prescribe the conditions, procedure and mode under which an application can be made and conditions subject to which LDC may be granted to the taxpayer. Continue reading “CBDT issues clarifications on relaxation for lower withholding certificates for tax years 2020-21 and 2019-20”

COVID-19 presents an unprecedented /extraordinary situation impacting the economic environment, which needs to be factored, while undertaking transfer pricing analysis of transactions effected during FY 2019-2020 and also in the next financial year. India is known to be one of the most aggressive Transfer Pricing (TP) jurisdiction. TP Team at Vaish Associates Advocates has noted the following issues, which would arise in TP arena, in the aftermath of COVID-19: Continue reading “COVID-19: Impact on Transfer Pricing Benchmarking”

Continue reading “FAQ’s – IMPACT OF COVID-19 ON LABOUR AND WORKFORCE”

In view of the unprecedented current situation arising out of the pandemic Novel COVID-19, the Ministry of Commerce and Industry issued a Press Release on March 31, 2020 announcing changes in the current Foreign Trade Policy (“FTP”) of the Government of India. Continue reading “FOREIGN TRADE POLICY EXTENDED DUE TO PANDEMIC COVID-19 BY ANOTHER ONE YEAR i.e. UP TO 31ST MARCH 2021.”